Weekly Market Commentary - April 19th, 2025 - Click Here for Past Commentaries

-

This past week, stock markets were modestly lower, with the S&P 500 down 1.5%, and the tech-heavy Nasdaq

down around 2.6%. For the full year, the S&P 500 is now down about 10.2%, while the Nasdaq is lower by

around 15.7%.

The move last week was driven once again by tariff uncertainty. New export restrictions on semiconductors

to China put pressure on large U.S. semi companies like NVIDIA. In addition, Fed Chair Powell reiterated

that the Fed is likely to remain patient on rate cuts, given that tariffs potentially weigh on both

inflation and economic growth.

Perhaps the good news was that the bond market last week functioned in a more orderly manner. As stocks

fell, government bond yields moved lower, with the 10-year Treasury yield lower by about 0.16% this

week alone, moving prices higher. The U.S. Agg bond index climbed about 1% for the week, providing

some diversification benefit for balanced investors.

Nonetheless, the broader markets continue to be driven by the tariff narrative in the near term.

Below we outline two different tariff scenarios – one with a moderate escalation in tariffs and

one with high tariff rates in place – and examine the impacts on key economic and market variables.

Overall, even a moderately higher tariff regime will negatively impact both inflation and economic

growth but perhaps can be offset by fiscal and monetary policy as we head toward 2026.

-

The moderate-tariff scenario is currently the highest probability outcome, in our view. In this scenario,

tariffs on most trading partners stay around 10%, with ongoing negotiations moving some rates and nontariff

barriers lower. The tariffs on China and critical sectors like autos, steel and aluminum likely remain

elevated; however, the negotiation between the U.S. and China is more productive and current tariff rates

could move lower. Overall, average tariff rates in this scenario are still around 10% to 15% in the U.S.

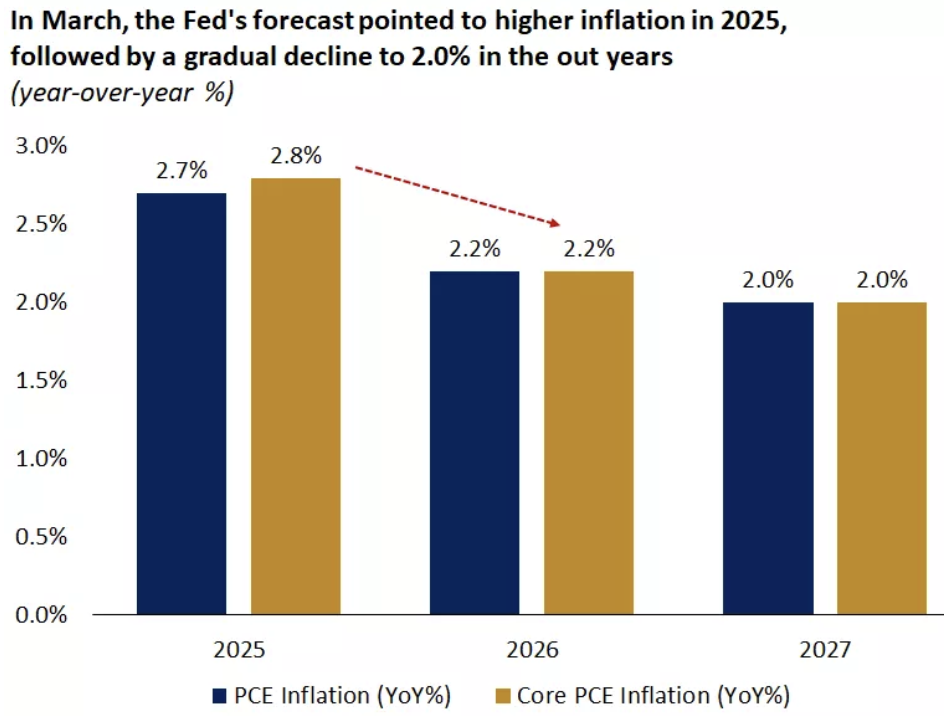

Economic growth and inflation: In this scenario, we would expect core CPI inflation to rise to 3.5% to 4%,

up from current levels of about 2.4%. We would expect inflation to gradually rise over the course of the

next few months, as companies work down existing inventories and replenish these at higher post-tariff

prices. However, while inflation may rise, we would expect it to peak this year and perhaps even move

lower by next year, as yearly comparisons ease versus this year's rise in prices. This is similar to

the inflation trend that the Fed outlined in its March 2025 meeting.

-

For economic growth, under a moderate tariff regime, we would expect the economy to slow, but growth

would likely remain positive this year, as households continue to spend on goods and services, albeit

at a softer pace. According to the 2018 Fed model, an increase in tariffs by 10% would imply a

softening in growth of about 1.4 percentage points, indicating growth may moderate to around 1%

annualized this year. While we may see a quarter of negative growth this year, we would not expect

a recession in the U.S. in the year ahead.

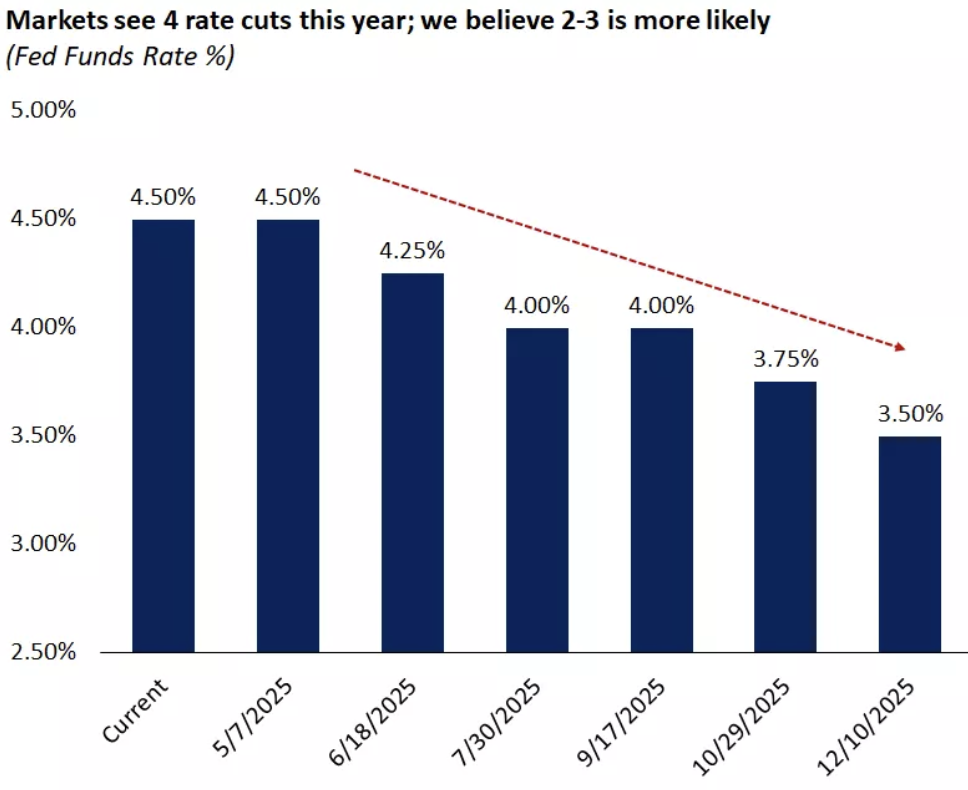

The Federal Reserve continues to be caught between "a rock and a hard place" as it navigates potentially higher inflation and lower economic growth. The Fed has already told us that it plans to remain patient as the data unfolds. In our view, inflation is likely to rise first, followed by a more pronounced slowdown in consumer and corporate spending, and then potentially higher unemployment and softer labor markets – typically a lagging indicator.

The Fed may act when it starts to see elevated tariffs impact the hard data, like consumer spending and ultimately lower GDP growth and higher unemployment. Given these will likely emerge more so in the back half of the year, the Fed may be on hold until the second half of 2025. We would expect the Fed to cut rates perhaps two or three times this year in this scenario, in line with the two rate cuts it outlined in the March meeting.

-

While we would not expect a V-shaped recovery from here in markets, we could see stabilization in the

months ahead. S&P 500 returns are typically driven by earnings and valuation expansion. In a

moderate-tariff scenario, we would expect S&P 500 earnings growth to be revised lower but still

remain positive in the low- to mid-single-digit range. If valuations are steady or even contract

a bit, this would imply flat returns for the S&P 500, which still is about 10% higher from

today's mid-April levels.

We would continue to expect to see diversified portfolios holding up relatively well, with the S&P 500 equal-weight index perhaps outperforming the market-weight index (which remains heavily skewed to growth and tech sectors).

In bonds, we would expect bond yields to remain range-bound, with 10-year Treasury yields in the 4.0% to 4.5% range. We could perhaps see yields approach the lower end of the range as the Fed moves rates lower toward the back half of the year. Nonetheless, with yields still in the 4% range, we continue to see bonds playing an important role in diversified portfolios.

-

There is still a chance that tariff rates remain meaningfully higher in the year ahead, although

this is a lower probability outcome in our view. In this scenario, the rates for China would

likely remain near peak levels, key sector tariffs remain elevated, and perhaps rates on some

trading partners move beyond 10% after the 90-day pause expires. In this case, the average tariff

rate in the U.S. moves closer to 25%.

Under this scenario, we would expect a more negative impact across most economic and market variables. Inflation would likely trend toward 5%, while economic growth would likely fall into recession. The Federal Reserve would also be more likely to cut rates sooner and more often, with four or five rate cuts likely.

From a market perspective, given a potential recession in this scenario, we would expect the S&P 500 to likely move back toward a bear market, down 20% or more from recent highs. In addition, bond yields would likely move lower, given a flight-to-safety response in the markets. We would expect 10-year yields to fall below 4.0% in this scenario. Overall, we would expect to see investors gravitate toward defensive positioning in both stock and bond markets.

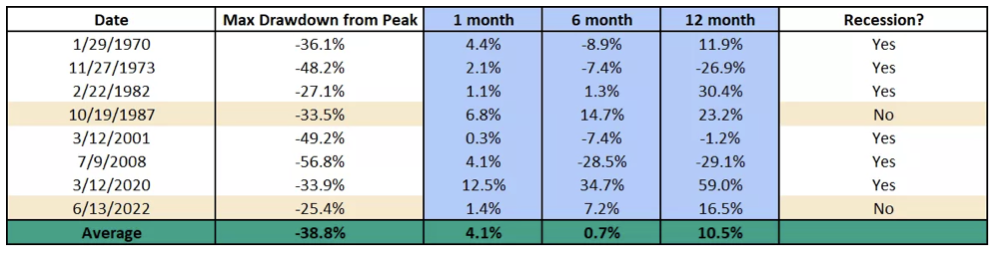

Since 1970, S&P 500 returns during a bear market have declined by an average of 39%, typically followed by a period of recovery:

-

While uncertainty remains high in the year ahead with elevated tariffs weighing on inflation

and growth, keep in mind that there may be some offsetting factors as we head through the year.

First, the administration has pointed to tax reform and deregulation as a key part of its agenda.

We would expect to see and hear more concrete plans for tax reform, and potentially lower taxes,

in the weeks ahead, which would provide fiscal support and improve market sentiment.

Second, we would expect the Federal Reserve to move rates lower over time, providing monetary stimulus to the economy. Lower interest rates would support better borrowing costs for consumers and corporations and help boost spending broadly. Remember that over time corporations can adapt to different operating environments, and sometimes innovation and productivity gains follow.

Overall, while this year may be fraught with tariff and trade volatility, we could potentially be setting up for a better 2026, with incremental fiscal and monetary stimulus supporting economic growth.

-

While market volatility is never comfortable, it is a normal part of investing. Keep in mind that in any

given year, two or three pullbacks are the norm, especially in years with heightened uncertainty. For

long-term investors, time in the market has consistently been proven to be a better strategy than

trying to time yourself in and out of the market, which can lead to poor investment decisions and

lower returns.

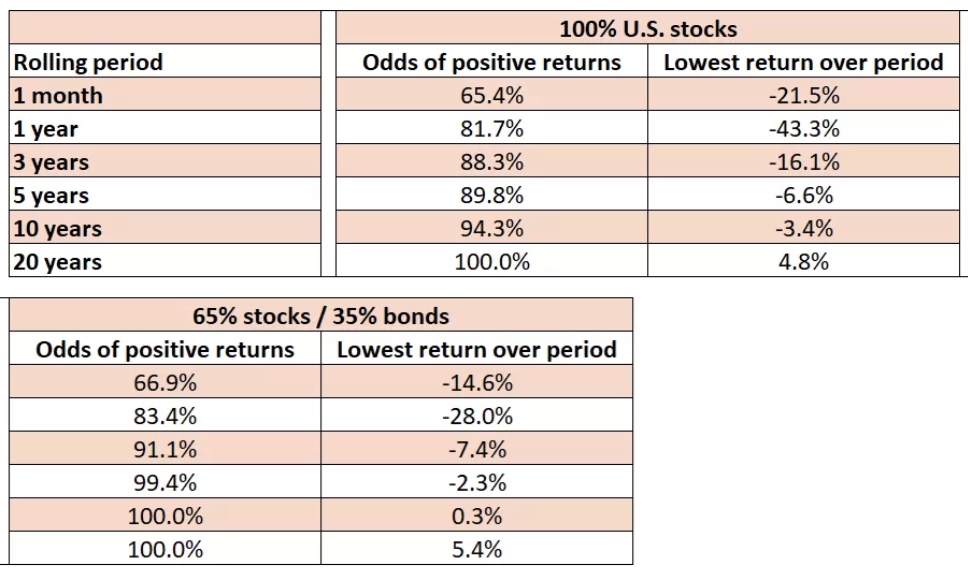

Instead, focus on what you can control. Work with a financial advisor to ensure you have appropriate emergency cash on hand. And from a portfolio perspective, consider opportunities to rebalance, diversify, or gradually add quality investments at better prices across asset classes and sectors. Remember that tariff uncertainty over time may shift, and we could see better economic and earnings growth in the year ahead. And over a 10 or 20-year horizon, annualized portfolio gains have a much higher probability of being positive than not.

-

Final Words: Markets are down and fed is going to cut

interest rate, greed warranted. Buy safety such as VOO and growth such as VGT. Balance.

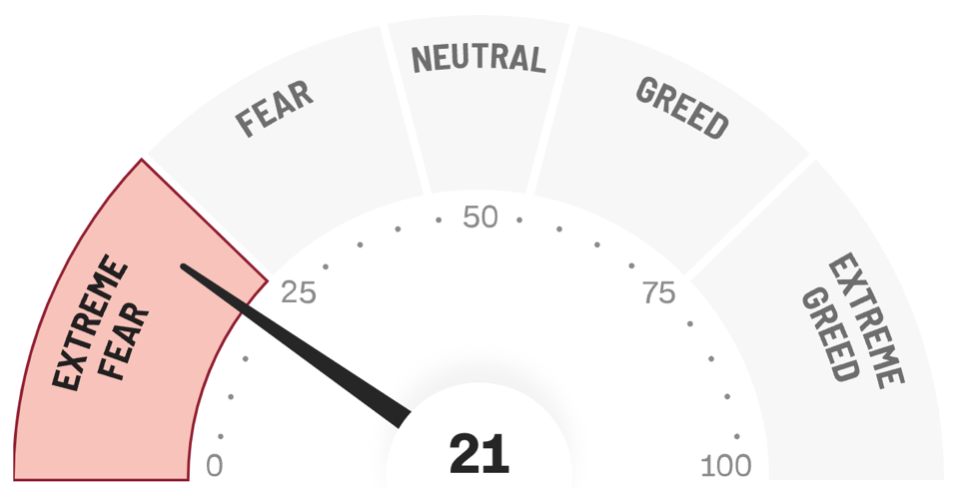

Below is CNN Greed vs Fear Index, pointing at 'Extreme Fear'.

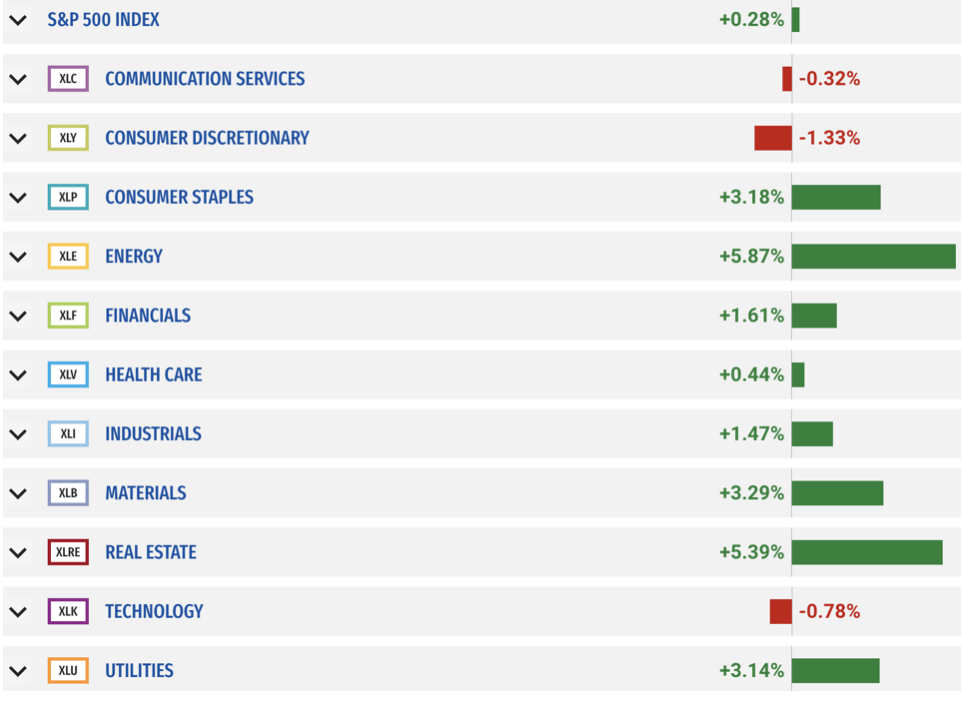

Below is last week sector performance report.

If you are looking for investment opportunities, you can take a look at our

Hidden Gems

section, and if you want to see our past performance, visit our

Past Performance section. If you are looking for

safe and low cost Exchange Traded funds(ETFs), check out our

ETF recommendations.

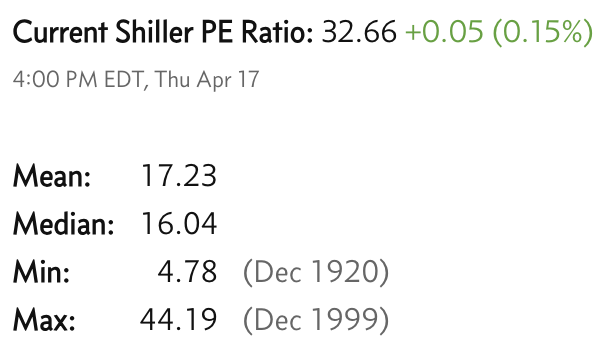

Currrent Shiller PE (see below) is showing overbought conditions as index is far above mean/media

and our AryaFin engine is indicating caution. Have a good weekend.